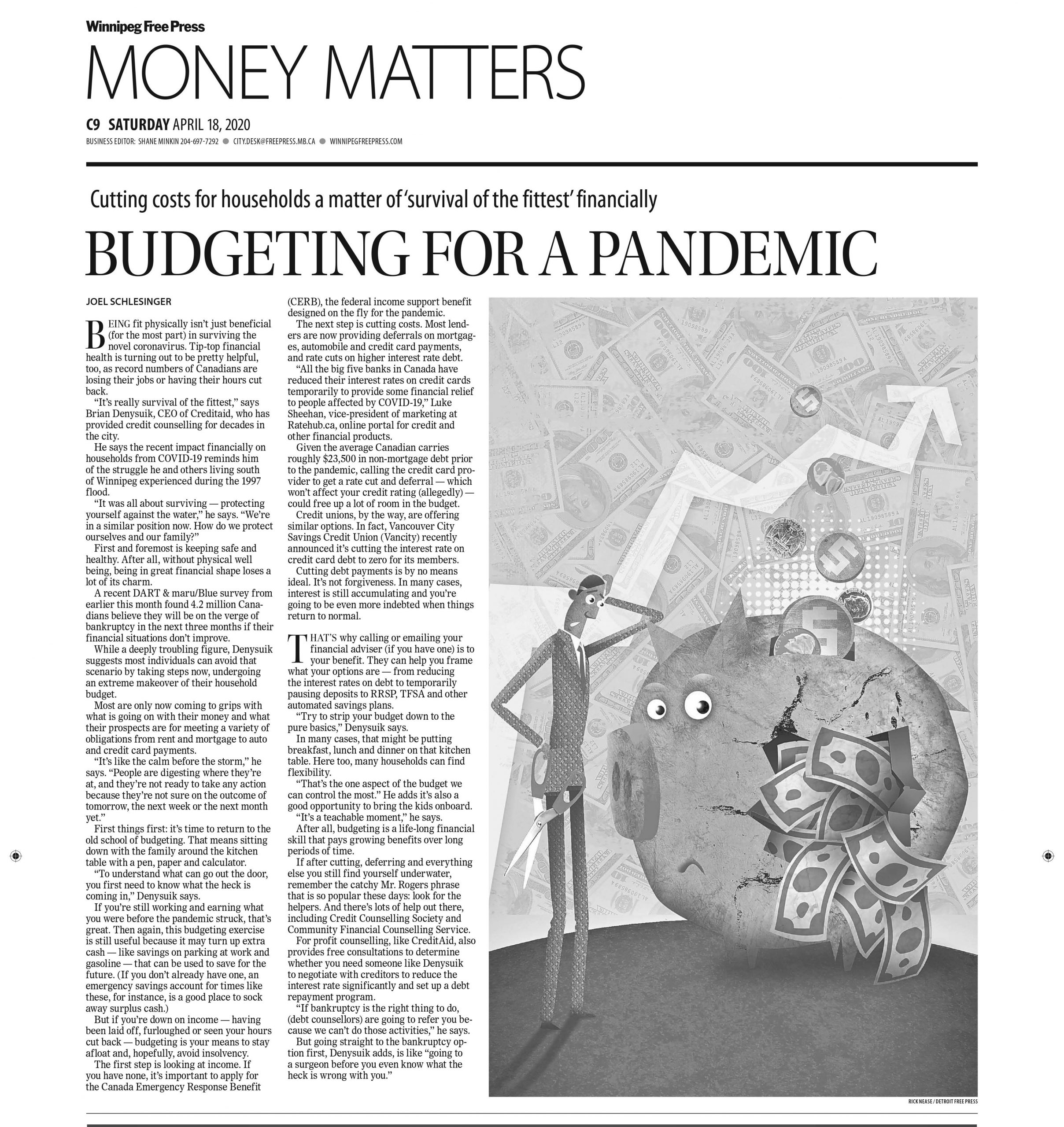

What do you think about when you hear the word budget? Does it send shivers down your spine? Do you immediately think of sacrifice and feeling restricted?

What if mastering budgeting skills could help you win at life? What if it could help you feel more at ease and have more freedom?

If you’re ready to win at your finances, check out the top budgeting skills you need below.

Record your Spending using a Paper or Electronic Transaction Register

You won’t know how much you have each month unless you track what is coming in and going out. It also helps keep you accountable. You’ll know when bills are due and what you owe. You’ll also know if you’re close to over-drafting your accounts and how much money you can save for emergencies or retirement.

Keep Track of Irregular Expenses

Even if you’re great at tracking your regular monthly expenses – those pesky irregular expenses can get you. Rather than letting them sneak up on you, write out all irregular expenses for the year. Think of expenses like Christmas spending, real estate taxes, annual insurance premiums, and home repairs.

Estimate the total cost of your irregular expenses and divide the total by 12 months. Put away at least this amount each month so that when the expenses come up, you’ll have the funds to pay it.

Get Good at Finding Deals

Shopping is a necessity, but you don’t have to overspend. Know when to buy products that you need, such as linens, clothing, appliances, furniture, mattresses, and cars. Time your purchases during the times these items are priced the lowest.

For example, furniture is usually the cheapest at the end of summer and end of winter; clothing is cheapest at the end of each season, and mattresses go on sale around each major holiday.

Shop with Lists

Shopping without a list, especially grocery shopping can be dangerous. Planning saves you money and stops you from buying things you don’t need.

Before you shop, create a meal plan for the week. Know what you’ll make for all meals and snacks. Plan your meals around the sales and/or coupons you have. If staple items you use often are on sale, stock up on them so you don’t have to pay regular price when you run out.

Avoid Impulse Buying

Impulse buying can send even the most thought out budget out the window. When something catches your eye, walk away from it. Give yourself 48 hours to think about it. If the item is still on your mind after 48 hours, consider the purchase, but do your research. Can you find it cheaper? Will there be a sale? Can you find a coupon?

Mastering these simple budgeting skills will help you stay on track financially. You’ll know when funds are low and you’ll see where you can cut back or make changes. Staying flexible and adaptable throughout the process will help you feel less restricted and even make you feel like you have more freedom to do what you want.

{kind=link}